|

Canadian Qualifying Mortgage Rate Lowered to 4.99%

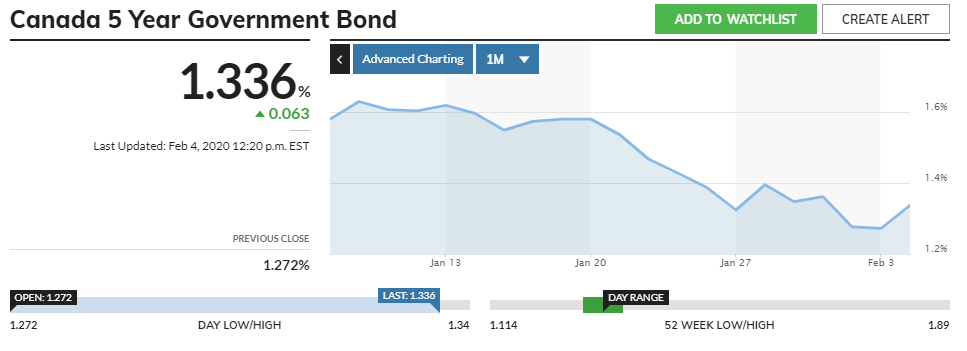

Market interest rates have fallen sharply since the coronavirus-led investor flight to the safety of government bonds. The 5-year government bond yield–a harbinger of conventional mortgage rates–now stands at 1.34%, down sharply from the 1.60+% range it was trading in before the virus became global news (see chart below).

This morning, one of the Big-Six banks finally reacted. TD cut its posted 5-year fixed rate to 4.99%. TD’s posted rate had previously been at 5.34%, making this a 36 basis point cut. Other banks had lowered their qualifying rate to 5.19% last July, leading the Bank of Canada to cut its 5-year conventional mortgage rate to 5.19%. This is the qualifying rate under the B-20 rule introduced on January 1, 2018.

Even the regulators have been questioning the efficacy and fairness of using the big-bank posted rate as a qualifying rate for mortgage stress testing.

On January 24, the Assistant Superintendent of OSFI’s Regulation Sector, Ben Gully, gave a speech at the C.D. Howe Institute suggesting that the B-20 qualifying mortgage rate historically would be no more than 200 basis points above contract rates. He said that OSFI chose the “best available rate at the time.”

He went on to say that for many years, the difference between the benchmark rate and the average contract rate was 200 bps. However, this gap “has been widening more recently, suggesting that the benchmark is less responsive to market changes than when it was first proposed. We are reviewing this aspect of our qualifying rate, as the posted rate is not playing the role that we intended. As always, we will share our results with our federal partners. This will help to inform the advice OSFI might provide to the Minister, as requested in the mandate letter to him.”

By keeping posted rates too high, the Big-Six banks have inflated the qualifying rate, making it more difficult than necessary to pass the stress test to get a mortgage.

While TD’s rate cut is welcome news, its posted rate is still too high by historical standards. Given today’s average contract rates, the posted rate should be at least 20 bps lower still.

Banks have a strong incentive to inflate their posted mortgage rate. For one thing, they are the basis for the calculation of big-bank mortgage penalties. Also, they are the minimum qualifying rate.

The posted rate does not appropriately reflect the state of the mortgage market as few borrowers would pay this rate. Interestingly, banks often move this rate in lock-step, or close to it, reflecting their dominant oligopolistic position in the marketplace.

If a couple of the other big banks follow TD’s lead, the Bank of Canada benchmark rate will be below 5% for the first time since January 2018 when the new B-20 rules were adopted. Lowering the stress test rate by 20 bps from 5.19% to 4.99% would require roughly 1.8% less income to qualify for a mortgage on the average Canadian home price (assuming a 20% downpayment), increasing buying power by 2%. This doesn’t sound like much, but it can have a meaningful psychological impact on already improving housing markets. The latest CREA data shows that the national average home price surged 9.6% year-over-year in December. A lower stress test rate would make a busy spring housing market even more active. |