|

||||||||||||||||||||||||||||

|

15

Oct

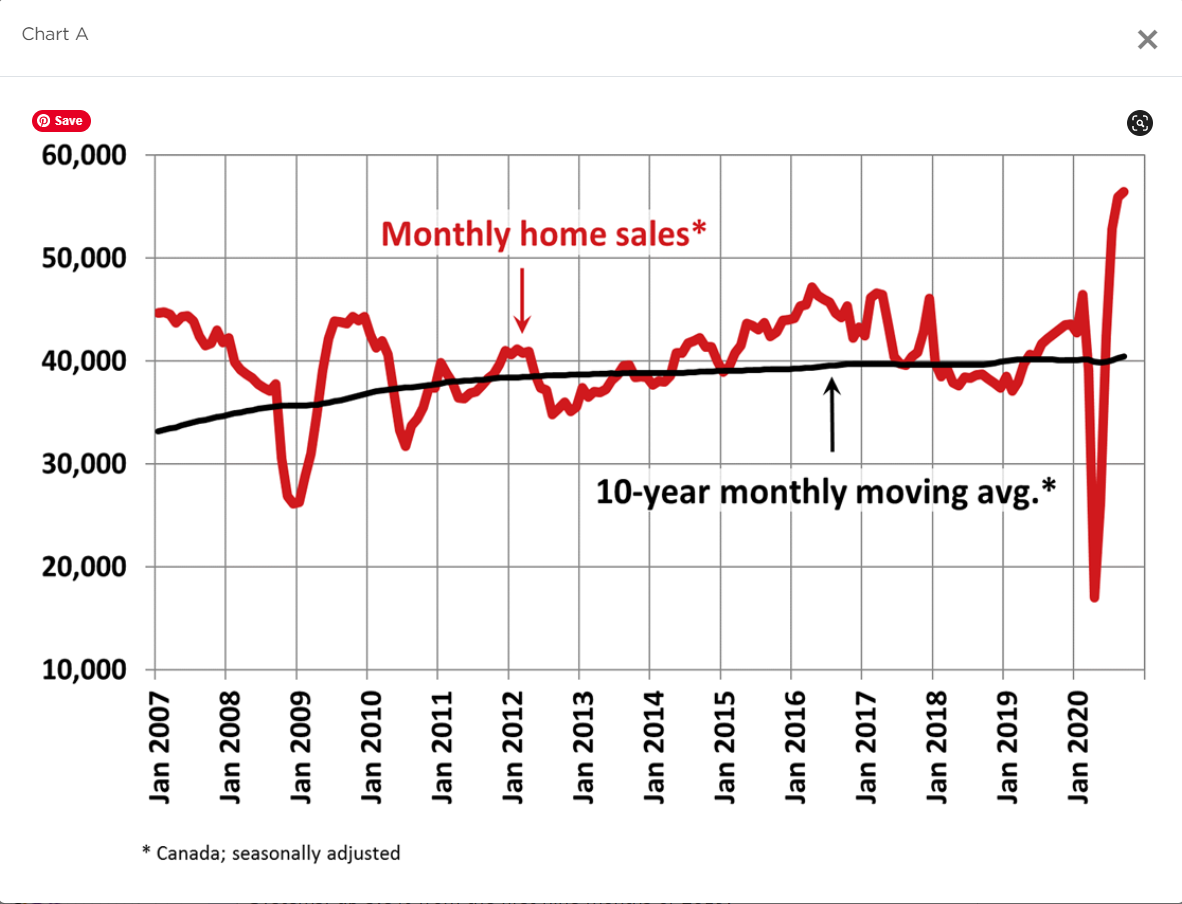

Home Sales Up

Posted by: Bill Yeung

Each Office Independently Owned & Operated

Posted by: Bill Yeung

|

||||||||||||||||||||||||||||

|

Posted by: Bill Yeung

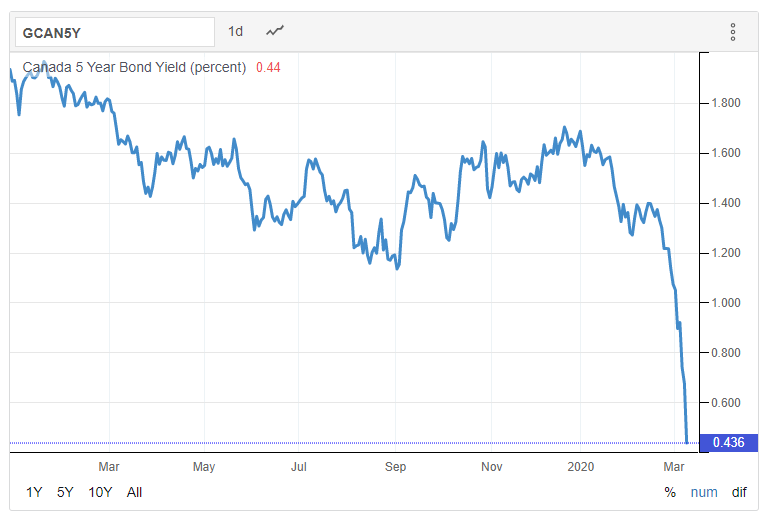

Following the Bank of Canada’s surprise announcement last week that it is lowering interest rates by 50 basis points to 0.75%, the country’s largest banks cut their prime lending rates to 2.95% from 3.45%.

Following the Bank of Canada’s surprise announcement last week that it is lowering interest rates by 50 basis points to 0.75%, the country’s largest banks cut their prime lending rates to 2.95% from 3.45%.

RBC Royal Bank, BMO Bank of Montreal, Toronto-Dominion Bank (TD Bank), Scotiabank, and CIBC slashed their prime rates – which underpins variable-rate mortgages and lines of credit – effective Tuesday, March 17. Meanwhile, National Bank of Canada will reduce its prime rate effective Wednesday, March 18.

Read more: Royal LePage CEO: BoC rate cut may act as a “relief valve” for overheated market

The Bank of Canada said that it cut interest rates, the second in two weeks, as a proactive measure “taken in light of the negative shocks to Canada’s economy arising from the COVID-19 pandemic and the recent sharp drop in oil prices.” The move was welcomed by several in the mortgage industry as a strong response to the uncertainty caused by these economic challenges.

“The Bank [of Canada] is acting forcefully to reduce the impact of the coronavirus on the economy,” said James Laird, co-founder of Ratehub.ca and president of CanWise Financial. “It is in these uncertain times that Federal institutions acting quickly and intelligently can reduce the negative impact of unforeseen events.”

However, some experts have warned that the same uncertainty will cause banks to hold back on passing the 50-basis-point rate cut to consumers.

In an email to BNN Bloomberg, Rob McLister, founder of mortgage comparison website RateSpy.com, said a slew of macroeconomic headwinds facing the big banks make him skeptical the lenders will pass along the 50-basis-point prime rate cut to consumers.

“What banks giveth with one hand they will taketh with the other by way of variable-rate discount reductions,” Rob McLister, founder of RateSpy.com, told Bloomberg News. “The weather forecast for banks is hurricane, tornado, and tsunami all in the same month. They’re getting sucker-punched by surging credit spreads, shrinking interest margins, rising loan loss reserves, and increasing default risk (even though mortgage arrears are little changed yet.)”

Posted by: Bill Yeung

Beginning today, the Bank of Canada is lowering its target for the overnight rate by 50 basis points to 0.75%. The Bank Rate is correspondingly 1 percent and the deposit rate is 0.50 percent.

The unscheduled rate decision is the second in as many weeks. In a statement, the central bank stated this was “a proactive measure taken in light of the negative shocks to Canada’s economy arising from the COVID-19 pandemic and the recent sharp drop in oil prices.”

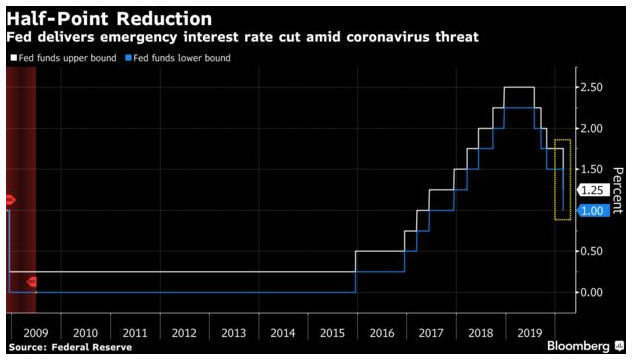

Last night, the US Federal Reserve made a surprise announcement in cutting its federal funds rate to a range of 0% to 0.25%. The US central bank also cited the negative economic impact from the coronavirus pandemic for its decision.

Separately, the Bank of Canada has teamed with five central banks to lower the pricing on the standing US dollar liquidity swap arrangements by 25 basis points.

Canada’s central bank announced on Sunday evening that it is working with the US Federal Reserve, the Bank of England, the Bank of Japan, the European Central Bank and the Swiss National Bank to ensure the new rate will be the U.S. dollar overnight index swap (OIS) rate plus 25 basis points. The central banks aim to increase the swap lines’ effectiveness in providing term liquidity by offering U.S. dollars weekly in each jurisdiction with an 84-day maturity, in addition to the one-week maturity operations currently offered.

These changes will take effect with the next scheduled operations during this week. The new pricing and maturity offerings will remain in place as long as appropriate to support the smooth functioning of U.S. dollar funding markets.

“The swap lines are available standing facilities and serve as an important liquidity backstop to ease strains in global funding markets, thereby helping to mitigate the effects of such strains on the supply of credit to households and businesses, both domestically and abroad,” said the Bank of Canada in a statement.

Posted by: Bill Yeung

The total value of residential sales in British Columbia increased by over 40% in February compared to the same month in 2019, according to figures from the British Columbia Real Estate Association (BCREA).

The total value of residential sales in British Columbia increased by over 40% in February compared to the same month in 2019, according to figures from the British Columbia Real Estate Association (BCREA).

BCREA reported that a total of 5,741 residential unit sales were recorded in February 2020, an increase of 26.3% from February 2019. The average residential price was $758,863, a 12% increase from $677,681 recorded the previous year. And significantly, the total sales volume in February was $4.4 billion – a 41.4% increase over 2019.

Read more: B-20 cost province $500 million in lost economic activity: BCREA

“Housing markets in BC continued to trend near long-term average levels in February,” said Brendon Ogmundson, chief economist at BCREA. “Recent declines in mortgage rates and favourable changes to mortgage qualifying rules may provide a boost to home sales heading into spring, although there is significant economic uncertainty lingering over the outlook.”

Total residential active listings fell 8.4% to 28,303 units compared to the same month last year. The ratio of sales to active residential listings increased 20.3% from 14.7% last February.

Perhaps unsurprisingly, the Greater Vancouver area experienced the biggest year-on-year sales increase with 2,185 residential unit sales – a 44.5% increase from last year. Additionally, the average residential price in Greater Vancouver was $1,006,708 – a 6.9% increase from the same period in 2019.

Posted by: Bill Yeung

|

Posted by: Bill Yeung

Yesterday’s unexpected announcement by the U.S. Federal Reserve to cut its benchmark interest rate in response to the economic uncertainty tied to the outbreak of the novel coronavirus (formally known as COVID-19) has convinced industry leaders that the Bank of Canada (BoC) will be forced to take a similar action today.

Yesterday’s unexpected announcement by the U.S. Federal Reserve to cut its benchmark interest rate in response to the economic uncertainty tied to the outbreak of the novel coronavirus (formally known as COVID-19) has convinced industry leaders that the Bank of Canada (BoC) will be forced to take a similar action today.

The emergency rate cut by a half percentage point to a target range of 1.00% to 1.25% was justified by the Federal Reserve as a necessary response to the economic risks posed by the coronavirus. The BoC is expected to announce its rate cut today from the 1.75% that has been in place since June 2015. The 1.75% benchmark interest rate is the highest among the G7 nations.

Following the news from the Federal Reserve, industry experts fanned out across the media to insist the only question related to a BoC rate cut would be the depth of the action.

“Twenty-five basis points may prompt loonie strength and derail the stimulus of the cut itself, while 50 basis points could stoke a housing bubble,” said Simon Harvey, FX market analyst for Monex Europe and Monex Canada, in a Reuters interview. “Markets are running with the fact that the latter is a less concerning risk at the moment and are aggressively pricing a similar 50 bps from the BoC,”

Although Canada has not experienced the abrupt increases in coronavirus cases that have been recorded in other countries, the economy is expected to feel an impact in certain sectors including travel and tourism, as well through disruptions in its global supply chain.

“That’s enough for them to cut on its own – the terms of trade shock, the travel and tourism, the supply chain disruptions from not being able to source inputs from China,” said Royce Mendes, an economist at Canadian Imperial Bank of Commerce in Toronto, in a Bloomberg interview.

Gareth Watson, wealth adviser at Richardson GMP, predicted the BoC will cut the benchmark interest rate a quarter percentage point.

“It will be a shocker to me if Canada doesn’t follow suit, considering Australia did this morning and there are expectations The Bank of England will follow suit this month,” said Watson in a CBC News interview.

Avery Shenfeld, chief economist at CIBC Capital Markets, told the Ottawa Citizen that a rate cut was long overdue.

“The Canadian economy was barely growing in the last quarter of 2019, so we’re putting a shock into the global economy at a time when Canada desperately was looking for momentum,” said Shenfeld.

And Derek Holt, economist at Bank of Nova Scotia, bluntly stated to the Wall Street Journal, “The Bank of Canada needs to cut. Now. Enough dithering.”

Separately, Prime Minister Justin Trudeau raised the possibility that the government would be willing to provide help to firms experiencing financial damage as a result of the coronavirus outbreak.

“There will be impacts on Canadian businesses, on entrepreneurs, and we will always look for ways to minimize that impact and perhaps give help where help is needed,” said Trudeau, although he did not offer specific details on the type of help or the possible qualifications for receiving assistance.

Finance Minister Bill Morneau took to Twitter to stress that Canadian actions related to the economic impacts of the coronavirus outbreak would be conducted in coordination with the other G7 countries, rather than in a domino effect of nation following nation in hurriedly adapting game plans.

“This morning I spoke with my G7 counterparts regarding the impacts on global economic activity from the COVID-19 outbreak,” Morneau wrote on Twitter. “We have reaffirmed our readiness to take action as necessary to aid in the response and support the economy. I’m continuing to monitor the issue closely.”

Posted by: Bill Yeung

|

|

|

|

|

Posted by: Bill Yeung

|

|

|

|

|

|

Posted by: Bill Yeung

|

Posted by: Bill Yeung

|

|

|

|

|

|